Financial Regrets

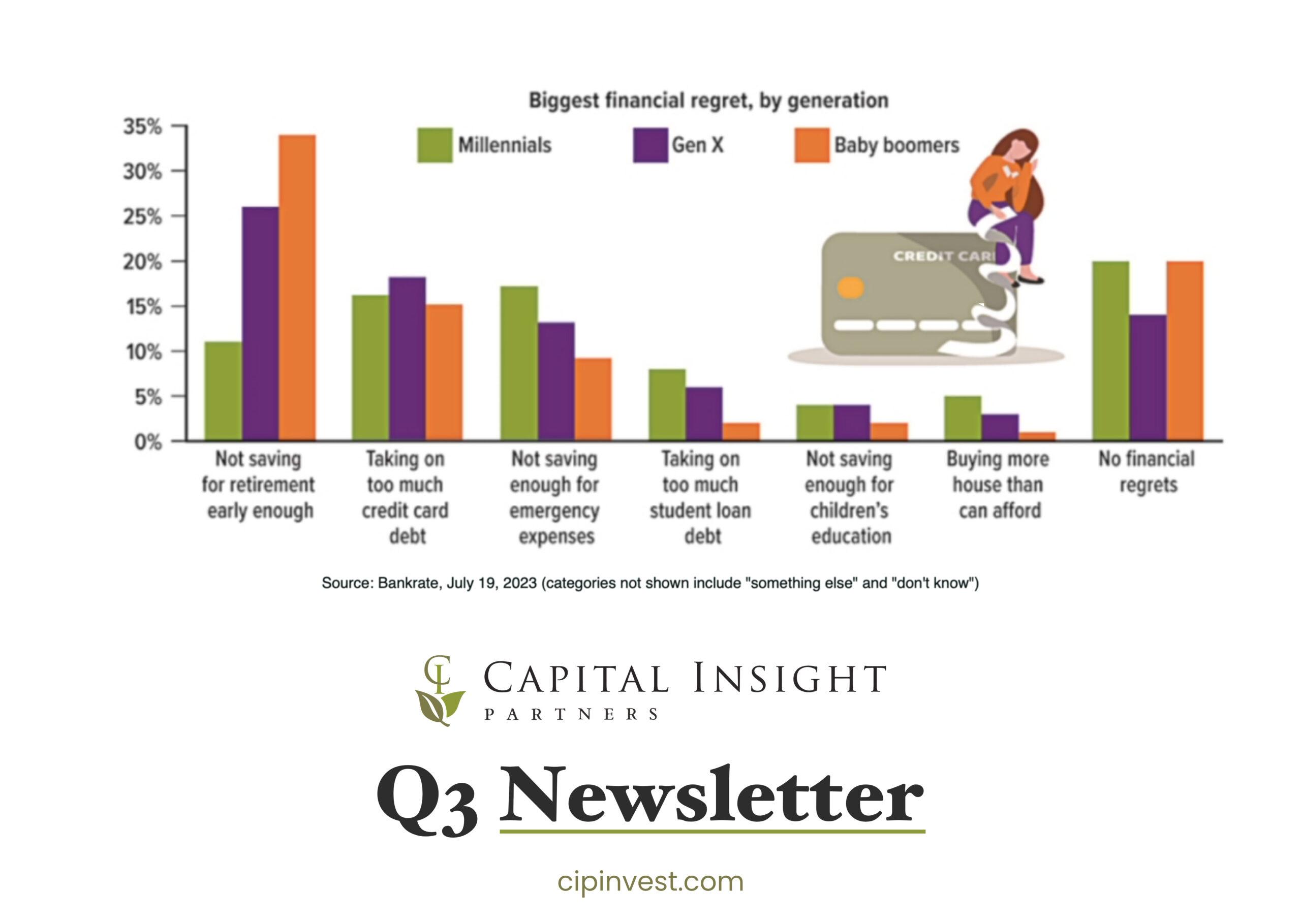

A 2023 survey found that about three out of four U.S. adults had a financial regret. The most common were not saving for retirement early enough, taking on too much credit card debt, and not saving enough for emergency expenses. It’s probably not surprising that the weight that people placed on these and other regrets varied by generation — and regret about not saving early enough for retirement was higher for those closer to retirement age.

37%

Percentage of workers with a workplace retirement savings plan who increased their contribution amount during the past year. By contrast, 11% of those with a plan decreased the amount but continued to contribute, and 4% stopped contributing.

Source: Employee Benefit Research Institute, 2023

Watch for These Hazards on the Road to Retirement

On the road to retirement, be on the lookout for hazards that can hamper your progress. Here are five potential risks that can slow you down.

Traveling aimlessly

Embarking on an adventure without a destination can be exciting, but not when it comes to retirement. Before starting any investing journey, the first step is setting a realistic goal. You’ll need to consider a number of factors — your desired lifestyle, salary/income, health, future Social Security benefits, any traditional pension benefits you or your spouse may be entitled to, and others. Examining your personal situation both now and in the future will help you home in on a target.

While some people prefer to establish a lump-sum goal amount — for example, $1 million or more — others find a large number daunting. Another option is to focus on how much you might need on a monthly basis during retirement. Regardless of the approach taken, be sure to factor in inflation, which can place unexpected curves in your path.

Investing too aggressively…

You may also encounter potholes when trying to target an appropriate rate of return. Retirement investors aiming for the highest possible returns might want to overweight their portfolio in the most aggressive — and risky — investments available. Although it’s generally wise to invest at least some of a retirement portfolio in higher-risk investments to help outpace inflation, the proportion and individual investment selections should be determined strategically. Investments seeking to achieve higher returns involve a higher degree of risk. Appropriate decisions will reflect your goal, your investment time horizon, and your general ability to withstand volatility.

Proceed with Caution

…Or too conservatively

On the other hand, if you’re afraid of losing any money at all, you might favor the most conservative investments, which strive to protect principal. Yet investing too conservatively can also be risky. If your portfolio does not earn enough, you may fall short of your goal and end up with a far different retirement lifestyle than you originally imagined.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

Giving in to temptation

Most people experience an unplanned detour on the road to retirement — the need for a new car, an unexpected home repair, an unforeseen medical expense, or the opportunity to take a long, exotic vacation.

During these times, your retirement portfolio may loom as a potential source of funding. But think twice before tapping these assets, particularly if the money is in a tax-deferred account such as an employer-sponsored plan or IRA. Consider that:

• Any dollars you remove from your portfolio will no longer be working for your future.

• In most cases, you will generally have to pay regular income taxes on amounts that represent tax-deferred investment dollars and earnings.

• If you’re under age 591⁄2, you may have to pay an additional penalty of 10% to 25%, depending on the type of retirement plan and other factors (some emergency exceptions apply — check with your plan or IRA administrator).

It’s best to carefully consider all other options before using money earmarked for retirement.

Prioritizing college over retirement

Many well-meaning parents may feel that saving for their children’s college education should be a higher priority than saving for their own retirement. “We can continue working as long as needed,” or “our home will fund our retirement,” are common beliefs. However, these can be very risky trains of thought. While no parent wants his or her children to take on a heavy debt burden to pay for education, loans are a common and realistic college-funding option — not so for retirement. If saving for both college and retirement seems impossible, a financial professional can help you explore a variety of tools and options to assist you in balancing both goals (however, there is no assurance that working with a financial professional will improve investment results).

Social Security 101

Social Security is complex, and the details are often misunderstood even by those who are already receiving benefits. It’s important to understand some of the basic rules and options and how they might affect your financial future.

Full retirement age (FRA)

Once you reach full retirement age, you can claim your full Social Security retirement benefit, also called your primary insurance amount or PIA. FRA ranges from 66 to 67, depending on your birth year (see chart).

Claiming early

The earliest you can claim your Social Security retirement benefit is age 62. However, your benefit will be permanently reduced if claimed before your FRA. At age 62, the reduction would be 25% to 30%, depending on your birth year. Your benefit may be further reduced temporarily if you work while receiving benefits before FRA and your income exceeds certain levels. However, when you reach FRA, an adjustment is made, and over time you will regain any benefits lost due to excess earnings.

Claiming later

If you do not claim your benefit at FRA, you will earn delayed retirement credits for each month you wait to claim, up to age 70. This will increase your benefit by two-thirds of 1% for each month, or 8% for each year you delay. There is no increase after age 70.

Spousal benefits

If you’re married, you may be eligible to receive a spousal benefit based on your spouse’s work record, whether you worked or not. The maximum spousal benefit, if claimed at your full retirement age, is 50% of your spouse’s PIA (regardless of whether he or she claimed early) and doesn’t include delayed retirement credits. If you claim a spousal benefit before reaching your FRA, your benefit will be permanently reduced.

Dependent benefits

Your dependent child may be eligible for benefits after you begin receiving Social Security if he or she is unmarried and meets one of the following criteria: (a) under age 18, (b) age 18 to 19 and a full-time student in grade 12 or lower, (c) age 18 or older with a disability that started before age 22. The maximum family benefit is equal to about 150% to 180% of your PIA, depending on your situation.

Survivor benefits

If your spouse dies, and you have reached your FRA, you can claim a full survivor benefit — 100% of your deceased spouse’s PIA and any delayed retirement credits. Note that FRA is slightly different for survivor benefits: 66 for those born from 1945 to 1956, gradually rising to 67 for those born in 1962 or later.

Claiming Early or Later

You can claim a reduced survivor benefit as early as age 60 (age 50 if you are disabled, or at any age if you are caring for the deceased’s child who is under age 16 or disabled, and receiving benefits). If you are eligible for a survivor benefit and a retirement benefit based on your own work record, you could claim a survivor benefit first and switch to your own retirement benefit at your FRA or later, if it would be higher.

Dependent children are eligible for survivor benefits, using the same criteria as dependent benefits. Dependent parents age 62 and older may be eligible for survivor benefits if they received at least half of their support from the deceased worker at the time of death.

Divorced spouses

If you were married for at least 10 years and are unmarried, you can receive a spousal or survivor benefit based on your ex’s work record. If your ex is eligible for but has not applied for Social Security benefits, you can still receive a spousal benefit if you have been divorced for at least two years.

These are just some of the fundamental facts to know about Social Security. For more information, including an estimate of your future benefits, see ssa.gov.

Can Home Improvements Lower Your Tax Bill? It Depends

Most home improvements are not tax deductible — with one possible exception. In certain situations, you may be able to deduct improvements deemed necessary for medical reasons (not just beneficial to general health). If you itemize instead of taking the standard deduction, you can deduct unreimbursed medical expenses that exceed 7.5% of your adjusted gross income, so the tax savings could be significant if a costly home improvement pushes your total medical expenses above that threshold. Installing air conditioning to help treat asthma or modifying a home to make it wheelchair accessible are common examples of qualifying expenses.

Here are two more ways that improving your home could potentially reduce your tax burden.

Capital improvements

Projects that add to the value of your home, prolong its life, or adapt it to new uses are considered capital improvements. When you sell your home in the future, you can add the cost of capital improvements to your initial basis (what you paid for it originally), reducing your capital gain and the resulting tax bill.

Some examples of capital improvements include remodeling the kitchen, replacing all your home’s windows, adding a bathroom, or installing a new roof. Repairs that keep your home in good condition (such as repainting, replacing a broken door or window, or fixing a leak) don’t count as capital improvements.

However, an entire repair job may be considered an improvement if it’s done as part of an extensive remodel or restoration.

Energy-saving tax credits

The Inflation Reduction Act of 2022 reconfigured two nonrefundable tax credits for home improvements that save energy. Unlike a deduction, which reduces your taxable income, a tax credit lowers your tax bill dollar for dollar. Both credits are available only for the installation of new products that meet specific energy efficiency requirements.

The energy efficient home improvement credit is equal to 30% of qualified expenditures for an existing home (not new construction). A $3,200 maximum annual credit is available through 2032. A $2,000 limit (30% of all costs, including labor) applies to electric or natural gas heat pumps, heat pump water heaters, and biomass stoves and boilers. A separate $1,200 limit applies to home energy audits and building envelope components (such as exterior doors, windows, skylights, and insulation) and energy property (including central air conditioners).

The residential clean energy property credit is a 30% tax credit available for qualifying expenditures for clean energy property (and related labor costs) such as solar panels, solar water heaters, geothermal heat pumps, wind turbines, fuel cells, and battery storage.

IMPORTANT DISCLOSURES Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.